NEW YORK and LONDON, Jan. 22, 2024 /PRNewswire/ — S&P Global Commodity Insights, the leading independent provider of information, analysis, data and benchmark prices for the commodities, energy and energy transition markets, has issued its latest report on the Top 10 Trends in Clean Energy Technology in 2024.

"Our forecast anticipates a 15% increase in clean energy technology (CET) investments in 2024 to nearly $800 billion, led by solar," says Philippe Frangules, Head of Gas, Power & Climate Solutions, S&P Global Commodity Insights. "Policy will continue to be the top driver of investments across CET, particularly for new technologies such as carbon capture and storage (CCUS), carbon dioxide removal (CDR) and hydrogen."

The report highlights an expected continued decline in the average cost of adding clean energy technologies to the worlds’ power grids, with a drop of 15% to 20% by 2030 and the call for a close watch on battery energy storage system manufacturing, which is becoming a "crowded space."

Global installations of wind and solar will reach one terawatt (TW) across the next two years, taking global installations to 3.5 TW and pressing an urgent need for more flexible power systems. "Any power system that is highly dependent on intermittent renewable generation will require increased flexibility assets such as storage and demand response," notes Edurne Zoco, Executive Director of Research and Analysis, Gas, Power & Climate Solutions, S&P Global Commodity Insights.

But it is offshore wind that is set for an "unprecedented milestone" year. "More than 60 gigawatts (GW) of new offshore capacity are set to be auctioned in at least 17 different markets − an all-time record high," emphasizes Eduard Sala de Vedruna, Clean Energy Technology Lead, S&P Global Commodity Insights. "Watch the degree to which the global wind turbine supply market remains bifurcated between China & the West and expect the clean-technology race to continue."

Find additional highlights of the report below:

TOP 10 TRENDS IN CLEAN ENERGY TECHNOLOGY IN 2024

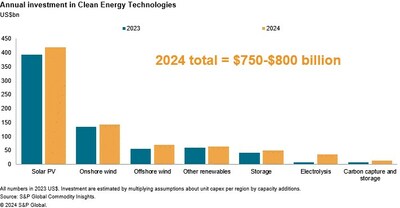

1. Clean Energy Technology Investment to reach nearly US$ $800 billion in 2024 and $1 trillion by 2030.

The S&P Global Commodity Insights forecast of nearly $800 billion in clean energy technology (CET) investments for 2024, if materialized, would be up 10% to 20% from 2023 spending levels. Solar will enjoy the largest share of the additional spend and account for some 55% of total investment. Onshore wind will be the second largest segment in terms of absolute investment, but it will grow more slowly. The fastest growing areas for new investments will be battery energy storage and electrolysis.

The first-ever mandate to store CO2 in Europe reduces uncertainties around the infrastructure needed for CO2 transport and storage and provides a positive signal to the global CCUS market, as does the enhanced 45Q tax credit contained in the US Inflation Reduction Act (IRA). A similar picture is emerging for hydrogen, with consumption mandates approved in Europe and auctions for support underway in Australia, India, the European Union and its member states, and the UK. The long-awaited publication in December 2023 of the highly contentious US Treasury guidance for the 45 V hydrogen production tax credit will define the investment framework in the US.

2. The average capex of clean energy technologies to decline by another 15%-20% by 2030

Despite rising costs of offshore wind and hydrogen, oversupply and falling raw material prices will ensure that the average cost of clean energy technologies continues to decline in 2024. The combination of oversupply and falling raw material prices is rapidly driving down the costs for solar and batteries from their 2022 highs. Costs came down significantly in 2023 and will drop well below 2020 levels in 2024.

More emerging technologies like green hydrogen and CCUS have seen the largest cost increases over the past two years, but they represent a very small share in total clean energy technology investment.

3. Clean energy technology manufacturers are making decarbonization core to both products & and strategies

The renewables industry, which has faced past scrutiny for selling components to generate low-carbon electricity while not similarly focusing on lowering the carbon footprint of the most energy-intensive parts of the value chain, is taking a new tack. Increasingly, renewables manufacturers are not only developing strategies to lower emissions at the core of their products, but have ambitious plans to decarbonize operations before 2030 as part of a bigger movement to increase the transparency and traceability of renewable supply chains and materials.

Decarbonization opportunities revolve around two key areas: 1) the use of low-carbon electricity resources like more renewables and hydroelectric-powered plants, and less coal or natural gas, and 2) a progressive reduction in materials consumption, such as of (e.g. polysilicon or silver), the exploration of less-intensive new manufacturing technologies, and use of lower carbon footprint materials.

4. Oversupply is driving solar and storage manufacturers into a price war – compressing margins and jeopardizing localization efforts

Solar and battery manufacturers enjoyed solid margins for two years but are facing lower margins through 2024. In solar, downstream players like distributors and installers are burdened by high inventories and face possible write-offs and higher financial risks due to declining prices. Oversupply and raw materials price drops in solar modules and batteries prompted a downstream price war in the second half of 2023 and will lead to market consolidation in 2024. Smaller manufacturers are likely to face negative gross margins, while leading large manufacturers will likely need to differentiate themselves through innovative products or exceptional price over quality decisions.

5. Expect record high offshore wind capacity auctions in 2024 despite rising capital costs

Despite the recent rise in costs of offshore wind due to supply chain bottlenecks and interest-rate-driven increases in financing costs, the upcoming year is poised to witness an unprecedented milestone. More than 60 GW of new capacity is set to be auctioned in at least 17 different markets − an all-time record in the realm of offshore wind energy, or enough to cover Poland’s total power demand. This surge in auctioned capacity serves as a resounding testament to the unwavering dedication of both established and emerging markets towards advancing and embracing this pivotal technology.

6. Western wind turbine giants face growing competition from the East

The global wind turbine supply market has been historically divided into two groups: approximately fifteen Chinese manufacturers supplying China domestically, and four regionally diversified Western firms largely catering to the rest of the world. But balance sheets of western turbine makers have weakened on high input costs, supply chain disruptions, mounting overheads, and onerous contracts. In contrast, Chinese turbine makers are increasingly competing against the Westerns in international markets through lower prices, technological innovation, and new supply chain investments.

China’s recently announced turbine production surpasses that of Western counterparts by at-least 30% in rated capacity, while the price gap has grown to nearly 70% between both groups. Expect the technology arms race and pricing pressure to continue, presenting Western turbine makers with the continued dual challenge of regaining profitability while safeguarding market share.

7. Expect higher global interest for low-carbon hydrogen as feedstock for ammonia, synthetic methane and synthetic liquids

Aided by subsidies and driven by mandates, investment in hydrogen as a feedstock is now flowing. In Denmark, green hydrogen production has been auctioned to green e-fuels and e-methanol facilities. The Danish results hint at possible similar outcomes of a broader EU auction through the European Hydrogen Bank that aims to provide €800 million of support to renewable hydrogen producers.

In the Middle East, a number of blue hydrogen and green hydrogen facilities are underway and aimed at meeting demand from Europe and/or Japan.

8. 2024 to be milestone year for technology-based carbon dioxide removal (CDR)

Rapid development of methodologies to verify carbon crediting and certify CDR, along with significant funding for technology-based removal, are driving the project pipeline to unprecedented levels (88 million metric tons per annum CO2 capture capacity under the current pipeline). CDR has been identified as a critical tool for achieving the climate targets, and buyers are willing to pay a premium for technology-based methods that are durable and easy to track.

The market is responding. Seven methodologies to verify carbon crediting from technology-based CDR have been announced. While the methodologies are still undergoing validation and verification, once finalized, they will provide a more rigorous carbon crediting estimation. The EU is expected to adopt a carbon removal certification framework in 2024.

Together, the crediting guidance and the growing demand for technology-based CDR are reducing uncertainty for potential buyers and will likely lead to a significant increase in projects in 2024. Government support and funding for CDR in Europe and the US will likely accelerate the trend. Projects that aim to capture biogenic and/or atmospheric CO2 are especially attractive due to restrictions on the CO2 sources that can be used for synthetic fuels.

9. Efforts to alleviate grid congestion and permitting constraints will continue to streamline renewable power development

One of the two major commitments to come out of COP28 is to triple global renewables capacity by 2030 to 11 terawatts (TW). The S&P Global Commodity Insights renewables outlook is aligned with this goal (using 2022 as baseline, and no major limitations or shortages foreseen from a material or supply chain perspective). Expect most of the renewable capacity additions to be solar, which is the fastest clean technology to install. Given solar’s intermittency and lack of sufficient storage capacity, solar additions of any major degree would only increase grid congestion and curtailment.

Grid-connection delays and grid congestion are becoming major bottlenecks for renewable deployment around the world, including delaying the build-out of energy storage that could help to address the problem. Globally, markets are expected to focus on two key means of reducing these bottlenecks and accelerating renewable build-out:

- Higher investment in transmission and distribution (T&D) and storage. The biggest factor behind grid-connection bottlenecks is that T&D investment lags generation capacity investment. This is a global phenomenon that is exacerbated in markets with higher renewable integration.

- Facilitation of development of other renewable technologies (e.g., offshore, geothermal), which have suffered from cost hikes and challenges in big interconnection and permitting.

10. Transmission system operators (TSOs) will be required to assess flexibility needs from 2025, which will drive additional large-scale energy storage procurements

More than 1 TW of wind and solar will be installed globally in the next two years, taking global installations to 3.5 TW and pressing an urgent need for more flexible power systems. A power system that is highly dependent on intermittent renewable generation (such as wind and solar PV) will require increased ‘flexibility’ to ensure that supply of electricity is balanced with demand. TSOs are taking action to ensure that flexibility assets such as storage and demand response will be available when needed. This trend was given a boost in March 2023 when electricity market design proposals stated that countries in Europe must evaluate their electricity systems’ flexibility requirements biannually, beginning January 2025. Such evaluations will include the capacity for non-fossil fuel-based flexibility, such as demand response and storage.

For more information on energy transition topics, visit: Energy Transition Service | S&P Global Commodity Insights (spglobal.com)

Media Contacts:

Americas: Kathleen Tanzy + 1 917-331-4607, kathleen.tanzy@spglobal.com

EMEA: Paul Sandell + 44 (0)7816 180039, paul.sandell@spglobal.com

Asia: Melissa Tan + 65-6597-6241, melissa.tan@spglobal.com

About S&P Global Commodity Insights

At S&P Global Commodity Insights, our complete view of global energy and commodity markets enables our customers to make decisions with conviction and create long-term, sustainable value.

We’re a trusted connector that brings together thought leaders, market participants, governments, and regulators and we create solutions that lead to progress. Vital to navigating commodity markets, our coverage includes oil and gas, power, chemicals, metals, agriculture, shipping and energy transition. Platts® products and services, including leading benchmark price assessments in the physical commodity markets, are offered through S&P Global Commodity Insights. S&P Global Commodity Insights maintains clear structural and operational separation between its price assessment activities and the other activities carried out by S&P Global Commodity Insights and the other business divisions of S&P Global.

S&P Global Commodity Insights is a division of S&P Global (NYSE: SPGI). S&P Global is the world’s foremost provider of credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity and automotive markets. With every one of our offerings, we help many of the world’s leading organizations navigate the economic landscape so they can plan for tomorrow, today. For more information visit https://www.spglobal.com/commodityinsights.

![]()

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/top-10-trends-in-clean-energy-technology-in-2024–sp-global-commodity-insights-302040712.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/top-10-trends-in-clean-energy-technology-in-2024–sp-global-commodity-insights-302040712.html

SOURCE S&P Global Commodity Insights

![]()